Page 20

DG 1110-3-126

August 1976

cost for a complete building. The percentages Iisted are

typical and taken from construction cost indices. They

may vary depending on local or special factors.

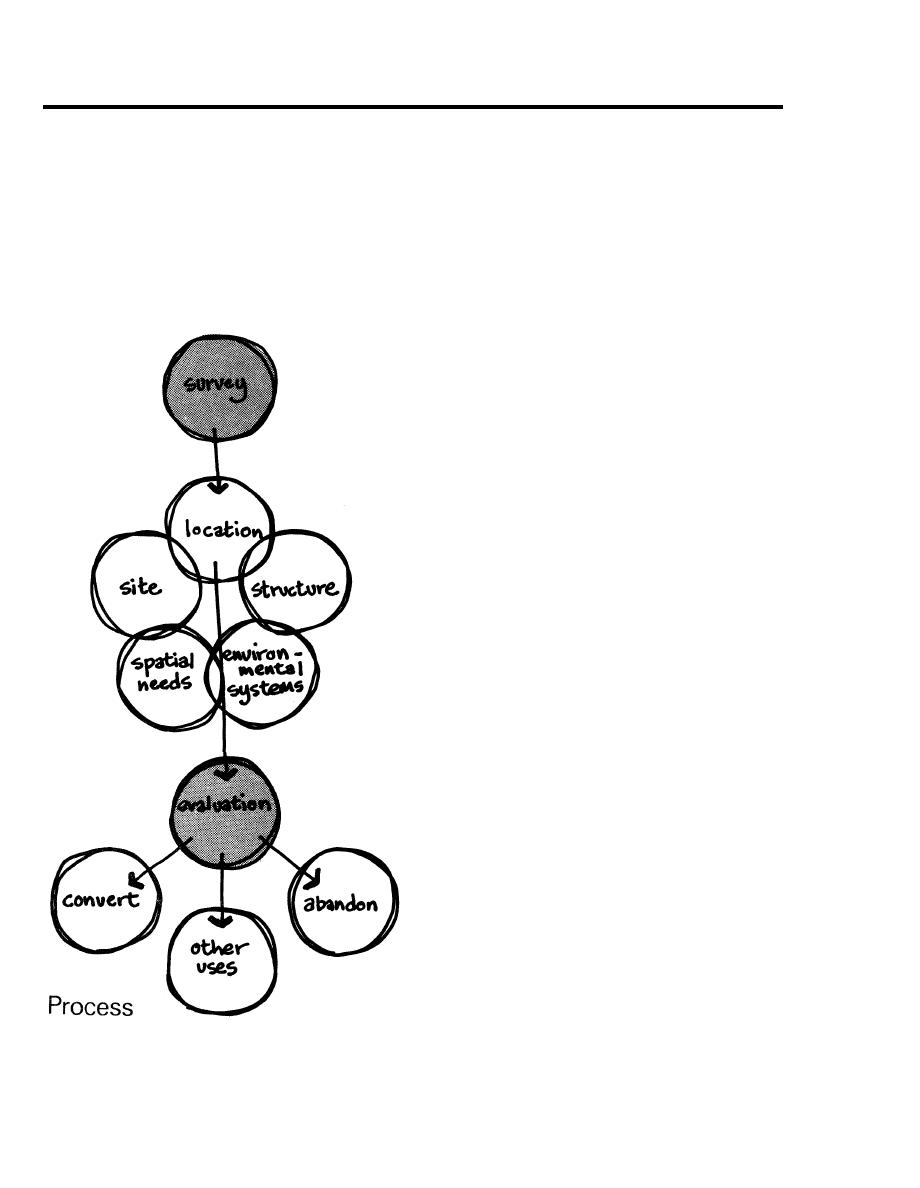

In most cases, a visual inspection by a knowledgeable

g.

surveyor, can result in a numerical value being assigned to

the percentage acceptable for each element. Those ele-

ments that are entirely acceptable are assigned a value, or

"feasibility factor" of 100. Those that require modifica-

tions are given lower numbers as are judged appropriate.

These are entered in column 3.

h. Column 4 provides an "Actual Value Factor". It is

determined by multiplying columns 2 and 3, and dividing

by 100. The total of all actual value factors produces an

overall value factor which offers a useful yardstick in

approximating the relative worth of an existing facility

compared to a new structure. One rule of thumb is that

if the overall value factor is over 50% it would be reason-

able to pursue in greater detail the economic feasibility of

converting its space. Simplified, that means, the existing

facility in its present state is worth half that of a new

physical facility. A sample evaluation is shown on the

chart.

i.

If the proposed facility has passed this test of accept-

ability, the next step is to establish preliminary cost esti-

mates for bringing the building to a state of usefulness for

its new function. This usually requires the preparation of

conceptual design drawings and an analysis of the useful-

ness of the converted space. Experience has shown that if

a building is converted to another use, it will usually have

to be larger than a building designed specifically for this

use, because of inherent problems of fIexibility and struc-

tural limitations.

Following the preparation of a program, a conceptual

j.

design response to it, and a preliminary cost estimate,

some valid judgments can be made on the advisability of

converting space. Obviously, if the cost of the conversions

are high in ratio to the Overall Value Factor the econom-

ics of conversion are highly suspect.

k. The initial cost of construction or of conversion

should not be the only economic criteria for decision

making. Life-cycle costing is a method of determining the

economic feasibility of facilities taking into account the

useful life expectancy of a converted facility against a new

one. It recognizes that initial cost is only one, and by no

means the largest, expense in a building's life. Operating

and maintenance costs are also considered. By amortizing

all costs over the life expectancy of a facility, a compara-

tive economic evaluation prorated on an annual basis can

be established. This then can form the foundation for eco-

nomic decisions.

Previous Page

Previous Page